A Guide to Car Rental Business Insurance

- fantasma70

- Dec 19, 2025

- 16 min read

Think of car rental insurance as a specialized type of commercial auto policy, built specifically for the unique chaos of the rental world. It’s not just a good idea—it’s the only thing standing between your business and a mountain of financial risk. Your personal auto policy won't touch a vehicle used for rentals, leaving you completely exposed to liability claims and fleet damage that could sink your company.

Why Your Rental Business Needs Specialized Insurance

Every time you hand over the keys, you're trusting a stranger with a high-value asset. You're also accepting the financial risk for whatever happens from the moment they drive off the lot. A standard business policy just isn't built for this, and as we mentioned, personal auto insurance becomes void the second a rental transaction occurs. This is where car rental business insurance becomes your most important investment.

This isn't just about playing it safe; it's a non-negotiable part of running a legal and sustainable operation. A single serious accident caused by one of your renters could easily trigger a lawsuit far exceeding the value of your entire fleet. Without the right coverage, that one incident could be a company-ending event.

Protecting Your Assets and Your Future

A solid insurance plan is your financial shield, custom-built to handle the daily risks of the rental game. It's designed for the messy, unpredictable situations that are totally unique to this industry.

Third-Party Liability: What happens when a renter hits another car, injuring the driver and totaling their vehicle? Your business could be on the hook for all of it.

Fleet Damage: Your cars face threats from everywhere. We're talking collisions, theft, vandalism, and even natural disasters—a very real concern for any business in Miami.

Renter Negligence: Sometimes, customers break the rules. They might drive recklessly or use the car for something prohibited in your agreement, leading straight to an accident.

Loss of Income: A car in the repair shop isn't making you money. Every day it's out of commission is a direct hit to your bottom line.

Think of it this way: Your fleet is the engine of your business. Car rental insurance is the bodyguard for every single vehicle, making sure one bad day doesn't shut down your whole operation.

To give you a clearer idea of how this all fits together, let’s look at the essential policies that form the bedrock of any good car rental insurance plan.

Essential Insurance for Your Car Rental Business

This table gives you a quick snapshot of the must-have coverages. Each one protects a different part of your business, and together, they create a comprehensive safety net for your rental fleet.

Coverage Type | What It Protects | Why It Is Essential |

|---|---|---|

Liability Insurance | Your business from claims if a renter causes bodily injury or property damage to someone else. | This is your frontline defense against crippling lawsuits and is required by law to operate. |

Physical Damage | Your actual vehicles against collision, theft, vandalism, and other direct damage. | It ensures you have the cash to repair or replace your cars, keeping your business running after an incident. |

Uninsured Motorist | Your business when your renter is hit by a driver with no insurance or not enough coverage. | It closes a dangerous loophole, so you're not left paying for damage caused by an irresponsible third party. |

These three coverages are the absolute foundation. Without them, you're driving blind and exposing your business to far too much risk.

Cracking Open Your Insurance Policy: What's Really Inside?

Opening your first car rental business insurance policy can feel a bit like trying to assemble furniture with instructions written in another language. It's packed with jargon and clauses, but don't let it intimidate you. Think of your policy less as a single document and more like a suit of armor—each piece is designed to protect a different part of your business from a specific kind of threat.

Let's pull back the curtain on the industry jargon and look at how each type of coverage actually works in the real world. Understanding this helps you see exactly what you're paying for and why every single component is critical to keeping your business safe and sound.

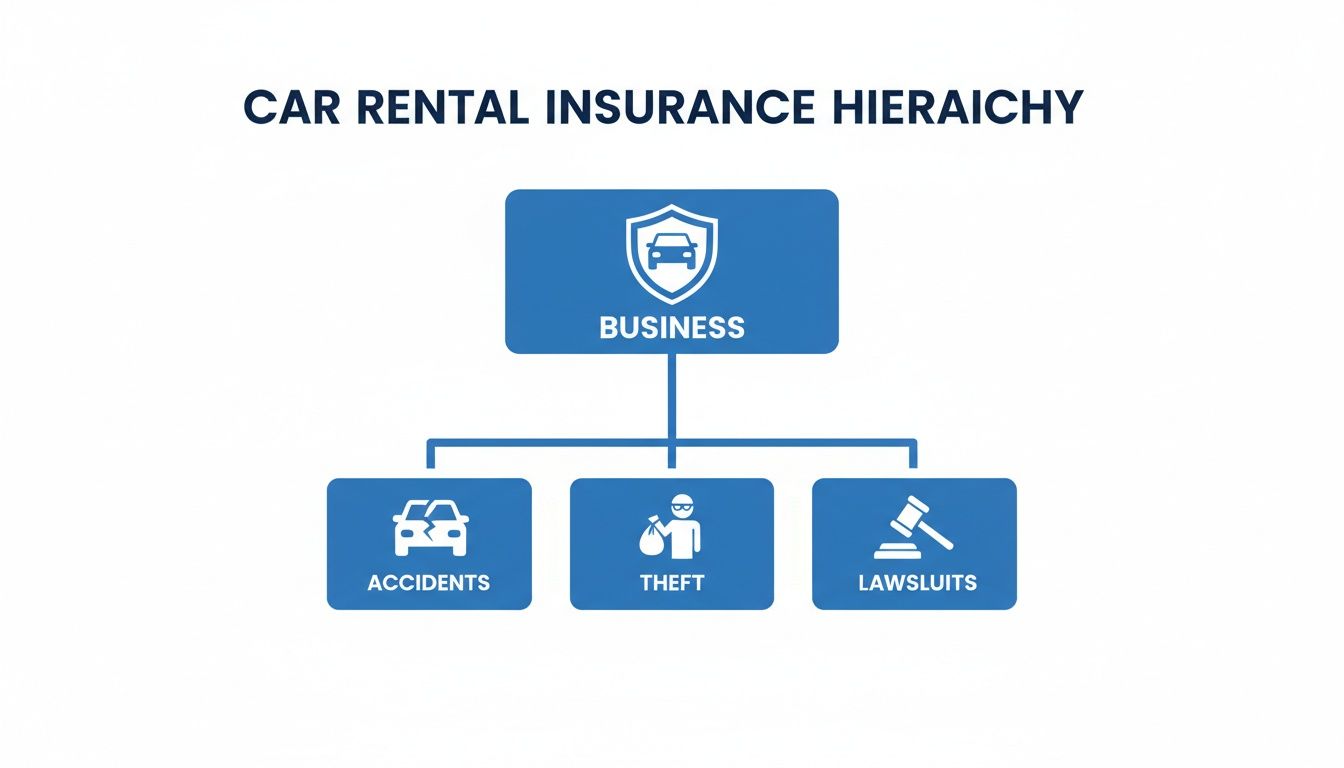

This diagram helps visualize how your main business insurance policy acts as a shield, protecting you from the big three risks: accidents, theft, and lawsuits.

From there, each risk branches out into specific situations, and that’s where the different types of coverage come into play to keep you financially whole.

Liability Insurance: The Foundation of It All

Liability insurance isn’t just a good idea; it’s the absolute bedrock of your entire policy. This is the coverage that kicks in when a renter gets into an accident and is found at fault for injuring someone or damaging their property. In nearly every state, this isn't optional—it's the law.

Picture this: a customer renting one of your SUVs glances at their phone and causes a three-car pile-up on a Miami freeway. Suddenly, you're facing multiple injuries and two totaled vehicles. The claims for medical bills and property damage could easily skyrocket into the hundreds of thousands, if not millions, of dollars.

Without solid liability coverage, your business is on the hook for every penny. With it, your insurance company steps up to manage the legal defense and pay the settlements, up to whatever limit you’ve chosen for your policy.

Your commercial liability insurance is your first and most important line of defense. Never assume a renter's personal policy will be enough. Your business policy has to be strong enough to handle the worst-case scenario all on its own.

Physical Damage Coverage: Protecting Your Actual Cars

While liability covers damage your renters do to others, physical damage coverage is what protects your own assets—your fleet. This coverage is generally split into two key parts that work hand-in-hand to guard your vehicles against almost anything.

Collision Coverage: This is straightforward. It pays to repair your rental car after an accident, whether it’s a minor fender bender or a serious crash. It doesn’t matter who was at fault.

Comprehensive Coverage: Think of this as the "anything but a collision" policy. It covers damage from a whole host of other problems: theft, vandalism, fire, hailstorms, or even a tree branch falling on a parked car.

So, if a renter parks a car for the night and it’s gone in the morning, your comprehensive coverage is what provides the money to replace it. This ensures one bad event doesn't permanently wipe a revenue-producing car off your books.

Uninsured and Underinsured Motorist Protection

Here’s a situation that happens more often than you'd think. Your renter does everything right, but they get hit by a driver who either has zero insurance or just the absolute legal minimum. What now? This is exactly where Uninsured/Underinsured Motorist (UM/UIM) coverage saves the day.

This protection steps in to cover your vehicle’s repairs and can also help with your renter’s medical bills if the driver who caused the accident can't pay. Without it, you’re stuck either eating the cost of repairs yourself or trying to sue someone who has no money—a battle you’re unlikely to win.

Supplemental Policies: Filling in the Gaps

Beyond the big three, a few other policies provide an extra layer of financial safety. They might not always be legally required, but for any serious rental operation, they are highly recommended.

Loss of Use CoverageOne of the most valuable yet overlooked coverages is loss of use. When one of your cars is stuck in the repair shop after an accident, it’s not out on the road earning you money. This coverage pays you for that lost rental income, keeping your cash flow steady while your asset is out of commission.

When you're trying to get a handle on different insurance policies, it can be useful to look at related concepts like motor truck cargo insurance, which defines liability for goods being transported. While the specifics are different, the core principle is the same: insuring against a specific kind of business interruption. For a car rental business, your "cargo" is the daily rental revenue, and loss of use coverage is what protects it.

Each of these coverages has a specific job to do. By layering liability, physical damage, and smart supplemental policies, you're building a financial structure that can handle the unpredictable nature of this business.

How Your Fleet's Insurance Premiums Are Calculated

Ever get an insurance quote and scratch your head, wondering how they landed on that number? It's not a shot in the dark. For a car rental business, calculating a premium is all about a deep-dive risk assessment by underwriters. Think of them as meticulous mechanics for your business's financial risk—they check every single component to figure out the odds of a claim and what it might cost.

The whole process boils down to a handful of key factors, from the cars on your lot to the streets they're driven on. Getting a handle on these elements does more than just explain the bill; it shines a spotlight on exactly where you can tighten things up to bring those costs down.

The Makeup of Your Fleet

First things first, an insurer is going to put your fleet under the microscope. The cars you rent are the heart of your operation and the primary assets they’re covering, so it’s no surprise their details have a huge impact on your rates.

Fleet Size: It's a numbers game. The more cars you have, the greater the overall exposure for the insurance company. A bigger fleet usually means a bigger premium, although you can often get a better per-vehicle rate as you grow.

Vehicle Type and Value: The kind of cars you offer is a massive factor. A lot full of luxury SUVs and high-end sedans will cost a whole lot more to insure than a lineup of dependable economy cars. Why? The math is simple: higher replacement costs and pricier repair bills for premium models directly inflate the cost of physical damage coverage. To see how different vehicle classes shape your business, check out these types of cars available for rent and think about their insurance implications.

Vehicle Age and Safety Features: Newer cars are often packed with safety tech like automatic emergency braking or lane-keeping assist, and insurers love that stuff—often rewarding you with discounts. On the flip side, older models without these modern protections can be flagged as a higher risk.

Your Operations and Location

Beyond the metal, insurers want to know how and where you do business. Your physical location can completely change your risk profile, as can the kind of drivers you attract.

It’s just common sense: a rental agency in a bustling urban core like downtown Miami, with its constant traffic and higher crime stats, is going to face steeper premiums than one in a sleepy suburban town. Insurers lean heavily on geographic data to weigh the local risks of collisions, theft, and vandalism.

Who you rent to matters, too. If your bread and butter is renting to seasoned business travelers, your risk profile looks much better than if you're primarily serving younger drivers or tourists who aren't used to the local roads.

At its core, an insurer's job is to predict the future by looking at the past. Your claims history is the clearest crystal ball they have, and a clean record is the best leverage you have for negotiating better premiums.

Claims History: The Ultimate Predictor

When all is said and done, your company’s claims history is probably the single biggest piece of the puzzle. It’s the most direct evidence of your real-world risk.

A track record dotted with frequent or expensive claims sends a clear signal to insurers: you’re likely to cost them money in the future. That translates directly into higher premiums.

But a clean slate? That tells a different story. A history with few or no claims proves you run a tight, safety-conscious ship, which can unlock serious savings and make insurance companies eager for your business. This is exactly why pouring resources into risk management—like solid driver screening and diligent vehicle maintenance—is an investment that pays for itself over and over again. By preventing incidents, you’re actively steering your insurance costs down.

Navigating State Laws and Airport Regulations

Beyond just protecting your cars and your bank account, your car rental business insurance is what makes you a legitimate, legal operation. The rules of the road for insurance aren't the same everywhere. It's more like a patchwork quilt of state, city, and even airport-specific regulations you absolutely have to follow.

Getting this wrong isn’t just a simple mistake. It can lead to massive fines, losing your business license, or getting kicked out of the most profitable locations, like airports.

Understanding State Minimum Liability Limits

Think of every state as having its own unique rulebook. The minimum liability coverage you're required to carry can change drastically just by crossing a state line. This is the absolute foundation of your commercial insurance policy.

For instance, Maine requires car rental businesses to carry at least $50,000 per person and $100,000 per accident for bodily injury liability. If your business is based there, your policy must meet those numbers at a bare minimum. Operating without it is like driving without a license—you're breaking the law.

It’s crucial to partner with an insurance agent who knows the specific rules for your state. They'll make sure your policy is compliant from the get-go.

However, these state minimums are just the starting line, not the finish line. A single serious accident can blow past those low limits in a hurry, leaving your business on the hook for the rest. That’s why savvy operators always buy policies with much higher limits than what the law strictly requires.

The High Stakes of Airport Operations

So, you want to operate at an airport? Get ready for a whole new level of scrutiny. Airports are high-traffic, high-risk zones, and the authorities that run them have their own set of non-negotiable insurance requirements designed to protect themselves.

State minimums won't even get you in the door. Airport authorities will almost certainly demand liability limits of $1 million or more, along with other special additions to your policy.

Additional Insured Endorsement: This is a classic airport requirement. It's a formal addition to your policy that names the airport authority as an "additional insured." This gives them a direct line to your insurance protection if a claim happens on their property because of your operations.

Simply put, without this endorsement, you won't get a permit to operate there. You'll also need to provide a Certificate of Insurance (COI), which is the official proof that your coverage meets their very specific and demanding standards.

Staying Compliant and Operational

Keeping up with these rules isn't a one-and-done task; it's a constant part of running your business. Laws change and airports update their requirements all the time. Here’s a simple game plan to stay on top of it:

Annual Policy Review: Make it a yearly habit to sit down with your insurance agent and review your policy against the latest state and local laws.

Check Airport Rules: If you're at an airport, check their requirements before you renew your policy each year. Don't get caught off guard by a change in limits or endorsement rules.

Find a Specialist: The best move you can make is to work with an insurance broker who lives and breathes commercial auto and car rental insurance. They know the ins and outs of these regulations.

Successfully managing the web of rules across different car rental locations is a cornerstone of a smart risk management plan. By understanding and following these requirements, you keep your business legally sound, fully protected, and ready for whatever comes next.

How to Reduce Risk and Lower Your Insurance Costs

Want to get a handle on your car rental business insurance costs? It’s not just about shopping around for the lowest quote. It's about actively managing your risk. Think of it this way: your insurance premium is a direct reflection of how safe an investment the insurer thinks your business is. The safer you operate, the less you'll pay. The good news is you have a ton of control over that perception.

This goes way beyond just saving a few bucks. A solid risk management plan protects your cars, your customers, and your company's good name. When you take these steps, you're not just cutting an expense—you're building a stronger, more profitable business from the inside out.

Implement a Rigorous Driver Screening Process

Your first and best line of defense is making sure you only rent to good drivers. Just glancing at a driver's license isn't enough. A truly effective screening process digs a little deeper to spot high-risk renters before you ever hand them the keys. Honestly, it’s the single most powerful thing you can do to prevent accidents.

You need a clear, consistent policy on who gets to rent from you. Here’s what that should look like:

Minimum Age Requirements: Set your age limit—often 25 years or older—to steer clear of statistically riskier young drivers.

Driving Record Checks: Run a motor vehicle report. You're looking for red flags like recent DUIs, reckless driving charges, or a collection of speeding tickets.

Valid License Verification: Seems obvious, but always, always confirm the license is valid, current, and not suspended.

If a driver looks like a risk on paper, they're going to be a risk on the road. Turning them away might feel like losing a sale, but trust me, it’s a tiny price to pay to avoid a five-figure insurance claim.

Leverage Technology to Monitor Your Fleet

These days, technology gives you a massive advantage in keeping your fleet safe. GPS and telematics systems aren't just for huge trucking companies anymore; they're essential tools for any rental operator who wants to protect their cars and promote safer driving.

Using telematics is like having a virtual co-pilot in every single car. It gives you the hard data to spot risky habits and protect your vehicles from being stolen or misused.

Think about equipping your fleet with these:

GPS Tracking: This is a no-brainer. It helps you get stolen cars back fast, which dramatically cuts the odds of a total loss claim.

Telematics Devices: These gadgets monitor how the car is being driven. They can flag things like hard braking, flooring the accelerator, and speeding, helping you identify renters who are abusing your vehicles.

Dash Cams: Installing a simple, front-facing dash cam provides crystal-clear evidence if an accident happens. It protects you from bogus claims and helps insurers figure out who was at fault without any guesswork.

Maintain a Rock-Solid Maintenance Schedule

A well-maintained car is a safe car. A blown tire or failing brakes can cause a wreck just as easily as a bad driver can. Being able to prove you have a strict maintenance program shows your insurance carrier you’re serious about keeping your fleet in prime condition.

Your routine maintenance checklist should always include:

Tires: Check air pressure and tread depth constantly.

Brakes: Regularly inspect pads, rotors, and brake fluid.

Lights: Make sure all headlights, taillights, and turn signals work perfectly.

Fluids: Keep oil, coolant, and washer fluid topped off.

Finally, your rental agreement is your ultimate safety net. It needs to be detailed and legally sound, clearly spelling out the renter's responsibilities, what they can't do with the car, and the consequences for breaking the rules. This document is your best friend in a liability dispute and helps protect your business when a renter does something they shouldn't.

A Step-By-Step Guide to Handling an Insurance Claim

So, one of your rental cars has been in an accident. Your heart sinks for a second, but what you do next can make all the difference. Having a clear, repeatable process turns the initial chaos into a manageable task and protects your business from unnecessary headaches.

The first few minutes after an incident are the most important. The priority is always safety, but right after that, it's all about gathering information. Think of it as building your case from the ground up.

What to Do at the Scene

You need a simple, non-negotiable checklist for your renters and staff to follow at the scene. This isn't just about ticking boxes; it's about protecting your assets and your bottom line.

Safety First: The absolute first step is checking if everyone is okay. If there are any injuries, call 911 immediately.

Become a Photographer: Pull out a phone and take pictures of everything. Get shots of the damage to all cars, the license plates, the entire scene from different angles, and even nearby street signs or skid marks. You can't have too many photos.

Collect the Details: Get the names, phone numbers, and insurance information from every single person involved. Don't forget to ask any witnesses for their contact info, too—they can be incredibly helpful later on.

Don't Admit Fault: This is a big one. Instruct your renters and team to state only the facts. Never, ever say "it was my fault." Let the insurance companies figure that out.

Report every incident promptly, even if it looks like a minor fender-bender. I've seen small claims snowball into major problems because they weren't reported right away. The longer you wait, the harder it is to piece together what happened, and your insurance carrier might start asking questions.

Filing and Managing the Claim

With the on-scene chaos handled, it's time to officially start the claims process. Staying organized here is your secret weapon for getting things resolved quickly and fairly.

Call your insurance provider as soon as you can and give them all the details you've collected. This gets the ball rolling and assigns an adjuster to your case. If you're new to this, getting a better understanding of insurance claims can give you a lot more confidence.

Keep a separate file for every single claim. Inside, you'll want the police report number, all your photos and videos, and a log of every conversation you have with the insurance company. This little bit of organization will be your best friend as you navigate your car rental business insurance claim.

Common Questions About Car Rental Business Insurance

When you're sorting out insurance for a car rental business, a few questions pop up time and time again. Getting clear, no-nonsense answers is the key to protecting your fleet and your finances. Let's break down some of the most common things rental operators ask.

One of the biggest, and most dangerous, misconceptions is about using personal insurance for a commercial business. Can you get away with it? Let's clear that up right now.

Can I Use a Personal Auto Policy?

The short answer? Absolutely not. Personal auto policies are written for one thing: personal, non-commercial driving. The second you hand the keys to a paying customer, you've stepped into the world of commercial operations.

Your personal insurance carrier will have language that specifically excludes this kind of commercial use. If a renter gets into an accident, any claim you file will be denied on the spot. That would leave you on the hook for potentially devastating liability and repair bills. You must have a dedicated commercial policy.

Fleet vs. Individual Vehicle Policies

Trying to insure each car in your rental fleet with a separate policy is a recipe for headaches and high costs. It just isn't practical.

That's where a fleet policy comes in. It’s designed to cover all of your vehicles under one umbrella policy, making it far more affordable and much easier to manage than trying to juggle individual plans. For any operation with more than a few cars, a fleet policy isn't just a smart move—it's the only real option.

A quick note on the Collision Damage Waiver (CDW): this isn't technically insurance. It’s a contract where you, the rental company, agree not to hold the renter financially responsible for damage in exchange for a fee. The risk essentially shifts back to your business, which is exactly what your commercial insurance policy is there to cover.

How Do I Verify a Renter's Insurance?

You can certainly ask customers to show you their personal insurance card, but relying on it is a huge gamble. There’s no quick way for you to confirm their coverage limits or check for tricky exclusions that might void coverage for a rental car. Their policy might not cover rentals at all, or they could have a massive deductible.

Because of this uncertainty, you can't depend on a renter’s policy to be your safety net. Your own commercial insurance is your first and most important line of defense. For more tips on navigating the ins and outs of the rental business, you can find a lot more information on the Cars4Go blog.

Ready to hit the road with confidence? At Cars4Go Rent A Car, we make renting in Miami simple and transparent. Book your vehicle today and experience the difference. https://www.cars4go.com

Comments