Florida Car Rental Insurance Requirements A Simple Guide

- fantasma70

- Feb 9

- 16 min read

So, you're renting a car in Florida. The big question at the counter is always about insurance. Do you really need to buy their expensive policy? The short answer is no, but you must have proof of liability coverage to drive off the lot.

You might already be covered through your personal auto policy or even your credit card. The trick is understanding Florida's specific rules to figure out what’s best for your trip.

Your Quick Guide To Florida Rental Car Insurance

Let's cut through the confusion. When you're standing at that rental counter, eager to hit the beach, insurance is probably the last thing you want to think about. But here’s the most important takeaway: while you can say "no thanks" to the rental company's insurance, you can't drive away without meeting Florida's minimum requirements. For a deeper dive into what can go wrong, understanding what happens when the car you're driving is a rental can be a real eye-opener.

Florida is a "no-fault" state. This just means that after an accident, your own Personal Injury Protection (PIP) policy is the first line of defense for your medical bills, no matter who was at fault. This system shapes the state's liability requirements, which you have to meet.

Making The Right Choice

Generally, you have a few ways to get covered. You can use your own car insurance, rely on benefits from a premium credit card, or buy a policy directly from the rental agency. Each path has its pros and cons. For example, your personal policy likely covers liability, but it might not pay for the rental company's "loss of use" fees while their car is in the shop.

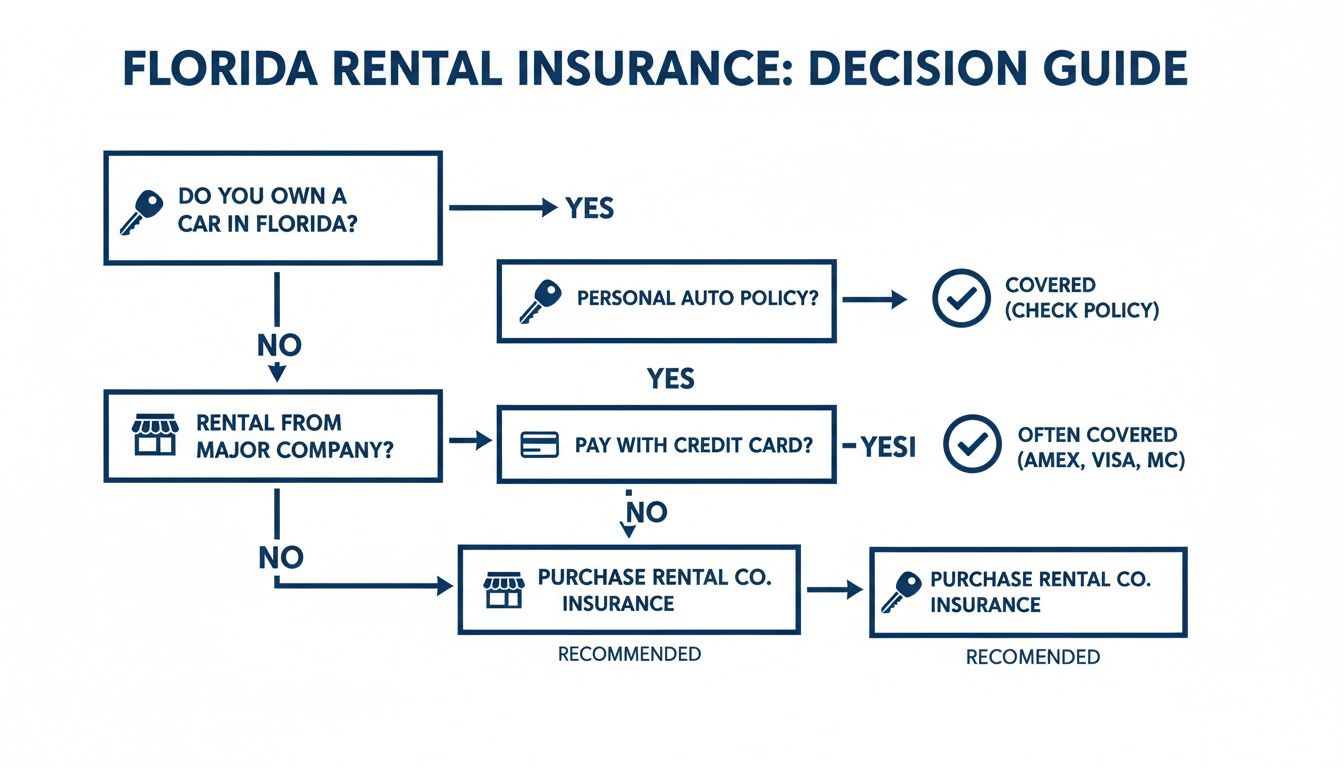

This decision-making flowchart breaks down the key questions to ask yourself.

It’s a simple visual to help you figure out if your current coverage is enough or if you need to add something extra at the counter.

Florida Rental Car Insurance Options At A Glance

To make it even clearer, here’s a simple breakdown of your main choices for rental car insurance in Florida. This table should help you quickly compare the options and see which one fits your situation best.

Coverage Option | How It Works | Typical Cost | Best For |

|---|---|---|---|

Personal Auto Policy | Your existing policy's liability and comprehensive/collision coverage may extend to rental cars. | $0 (included in your premium) | Domestic renters with comprehensive personal policies. |

Credit Card Benefits | Many premium travel cards offer secondary (or sometimes primary) rental car collision damage waivers. | $0 (included with card) | Renters who already have liability coverage but want extra protection for damage to the rental vehicle. |

Rental Company Insurance | You buy coverage like a Loss/Collision Damage Waiver (LDW/CDW) or Supplemental Liability directly at the counter. | $15 - $50+ per day | International visitors or anyone without personal auto insurance or adequate credit card benefits. |

Third-Party Insurance | You purchase a standalone policy from an independent insurance provider before your trip. | $5 - $15 per day | Travelers who want to avoid high rental-counter prices but need comprehensive coverage. |

Ultimately, having a plan before you get to the airport will save you stress and money. A quick call to your insurance agent or credit card company can clear up any confusion.

Florida's Minimum Requirements Explained

Here’s what the law actually says. Florida doesn't require you to buy the rental company's policy, but it does mandate that every car on the road has minimum coverage.

This includes:

$10,000 in Personal Injury Protection (PIP)

$10,000 in Property Damage Liability (PDL)

If you can't show proof that you have this coverage from another source (like your own policy), the rental company has to sell you a liability package. They can't legally let you drive away without it.

Here's the bottom line: Proof of insurance is non-negotiable. Walking up to the rental counter with your insurance card or policy details in hand will prevent a last-minute scramble and protect you from buying overpriced coverage you might not even need.

Understanding Florida’s Unique Insurance Landscape

Renting a car in the Sunshine State can feel a little different, and that's because its insurance laws are built on a unique foundation: the “No-Fault” system. Getting a handle on this one concept is the key to understanding everything else.

So, what does "no-fault" actually mean? In a nutshell, it changes how medical bills get paid right after an accident.

Imagine a simple fender bender. In most states, the next step is a blame game to figure out whose insurance company has to pay for injuries. Florida’s no-fault law cuts through that initial red tape. Your own insurance policy is the first one to cover your medical costs, up to a certain limit, no matter who was responsible for the crash.

The whole point is to get people paid for minor injuries faster and keep smaller accidents from clogging up the court system. This core idea is what shapes the florida car rental insurance requirements you'll face at the counter.

The Two Pillars of Florida Auto Insurance

Thanks to this no-fault system, Florida law mandates that every registered vehicle carry two specific coverages. Think of them as the non-negotiable building blocks for any car insurance policy here. Knowing what they are is crucial for making a smart choice when you rent.

Here are the two must-haves:

Personal Injury Protection (PIP): This is the heart and soul of the no-fault law. It covers 80% of your initial medical bills and 60% of any lost wages, up to a limit of $10,000, regardless of fault. It’s your immediate financial safety net.

Property Damage Liability (PDL): This policy pays for damage you cause to other people's property. If you hit another vehicle, a fence, or a mailbox, your PDL steps in to cover those repairs, up to a $10,000 minimum.

What's really important to notice here is what's missing. Florida law does not require Bodily Injury Liability (BIL), which pays for injuries you cause to other people in an accident where you're at fault. This is a huge departure from most states and creates a major potential gap in your coverage.

How No-Fault Affects You as a Renter

Okay, so what does this all mean when you just want to rent a car for your vacation?

While the rental car itself is legally insured by the company, the burden of proof is on you—the driver—to show you have enough coverage to protect others.

It's a common mistake to think the rental company's basic insurance has you fully covered. The reality is, their state-required minimums are quite low and exist mainly to protect their business, not you as a driver. Relying solely on their base plan could leave you in a serious financial bind.

If you don't have a personal auto policy that works for a rental in Florida, you'll have to buy liability coverage directly from the rental agency. This is non-negotiable. It ensures there's a policy in place to pay for any property damage you might cause.

The rental agent will ask to see proof of your coverage, which is usually just your insurance ID card or the declarations page of your policy. If you can't provide it, you won't be able to drive off the lot without purchasing their liability protection first. This is why getting to know Florida's unique rules isn't just about protecting the car—it's about meeting the law and protecting your wallet.

Decoding The Rental Counter Insurance Options

You finally make it to the rental counter, ready to grab your keys and go. But then you're hit with a rapid-fire list of confusing acronyms: LDW, CDW, SLI, PAI. It can feel like a high-pressure sales tactic, but understanding what these options actually do is your best defense.

Think of the insurance offerings at the counter as an à la carte menu. You only need to pick what fills the gaps in your existing coverage from your personal auto policy or credit card.

Let's break down the jargon.

Loss Damage Waiver and Collision Damage Waiver

The first thing you’ll almost always hear about is the Loss Damage Waiver (LDW), sometimes called a Collision Damage Waiver (CDW). Here’s the key thing to know: this isn't technically insurance. It’s a waiver.

By accepting it, the rental company agrees not to come after you for the cost of damage or theft.

Imagine a stray palm frond scratches the paint, or a rogue shopping cart dings the door. With an LDW, you can just hand back the keys and walk away without worrying about repair bills, administrative fees, or the dreaded "loss of use" charges while the car is in the shop.

Be careful, though. An LDW has fine print. Things like driving under the influence, using the car for a delivery service, or taking it on unpaved roads can void the agreement entirely, leaving you on the hook for every penny of damage.

Supplemental Liability Insurance

Next up is Supplemental Liability Insurance (SLI). This is a big one, especially in Florida. As we covered, the state’s minimum liability requirement is a shockingly low $10,000 for property damage.

It doesn’t take much for a minor fender-bender to blow past that limit. SLI is your safety net, boosting your liability protection up to $1 million in many cases. It covers the damage you might cause to other people’s cars and property, along with their medical bills if you’re found at fault. When considering what to buy, it's crucial to know what liability insurance covers since it protects you from the biggest financial risks.

For international visitors or even U.S. travelers with bare-bones liability on their personal policy, SLI is a must-have. A serious accident can have devastating financial consequences, and this coverage provides a powerful shield.

When you're planning your trip, picking the right vehicle is just as important as sorting out your insurance. You can explore different models on our page showing all available car types.

Personal Accident and Personal Effects Coverage

Finally, you'll probably be offered a bundle of two smaller coverages:

Personal Accident Insurance (PAI): This helps pay for medical costs for you and your passengers after a crash. If you already have good health insurance or PIP on your own car insurance, this is often an unnecessary expense.

Personal Effects Coverage (PEC): This insures your stuff—like a laptop or luggage—if it's stolen from the rental car. Most homeowners or renters insurance policies already cover your belongings when you travel, so check that first.

For most people, these last two are redundant. Always double-check your existing policies before you leave home to avoid paying for coverage you don’t need.

Rental Counter Insurance Explained

Still feeling a little overwhelmed? Here’s a simple table to help you keep these options straight when you're standing at the counter.

Insurance Type | What It Covers | Typical Daily Cost | Key Consideration |

|---|---|---|---|

LDW / CDW | Damage, theft, or vandalism of the rental car itself. | $10 - $30 | Your personal auto policy or credit card may already provide this. |

SLI | Damage to other people's property and their medical bills. | $10 - $20 | Essential if you have low liability limits or are an international visitor. |

PAI | Medical expenses for you and your passengers after an accident. | $2 - $7 | Often redundant if you have health insurance or PIP. |

PEC | Theft of personal belongings from the rental car. | $1 - $5 | Your homeowners or renters insurance likely covers this already. |

The global market for rental car insurance shows just how important this is to travelers. Valued at $937 million, it's expected to hit $1,282 million soon, growing at 6.8% annually. This tells us that more people are realizing they need solid protection. By understanding these options, you can make a smart, confident decision and avoid paying for anything you don't truly need.

Using Your Own Insurance and Credit Card Perks

Before you hand over your credit card for the rental company’s expensive insurance, take a minute to look at what's already in your wallet. There’s a good chance you already have some coverage through your personal car insurance or the credit card you’re using to pay for the rental.

This is one of the easiest ways to save a significant amount of money. But—and this is a big but—you can't just assume you're covered. You need to do a little homework first to see what your policies actually cover and, just as importantly, what they don't cover for a rental car in Florida.

Your Personal Auto Policy: The First Place to Look

For most drivers from the U.S., your own car insurance is the natural starting point. If you have comprehensive and collision on your personal vehicle, that coverage usually follows you when you get behind the wheel of a rental. In simple terms, if you ding the rental, your own policy will cover the damages, minus your usual deductible.

Sounds great, right? It is, but personal policies often have some sneaky gaps. For instance, many won't cover the rental company’s "loss of use" charges, which is the money they claim they're losing while the car is stuck in the repair shop. They might also stick you with administrative fees or the "diminished value" of the car after it's been in a wreck.

Here's a common mistake we see all the time: assuming your personal liability coverage is enough. If you only have the state minimums on your own car, a serious accident in a rental could leave you exposed. Renting a car is a good excuse to double-check that your liability limits are up to snuff.

The Hidden Power in Your Plastic: Credit Card Benefits

Many travel rewards credit cards come with a fantastic perk: rental car insurance. The catch? Not all coverage is created equal. It generally comes in two flavors, and knowing the difference is key.

Secondary Coverage: This is the most common type. It only kicks in after your personal car insurance has paid its share. Think of it as a safety net that helps cover things your main policy misses, like your deductible.

Primary Coverage: This is the gold standard, usually found on premium travel cards. It steps in first, so you don't even have to file a claim with your personal insurer. This is a huge benefit because it can save you from a potential rate hike on your personal policy.

Even with the best primary coverage, there are always rules. Most cards exclude certain vehicles (think luxury cars, exotic sports cars, or large passenger vans), rentals that last longer than 15 or 30 days, and they almost never include any liability protection. It's strictly for damage to the rental car itself.

Your Pre-Trip Insurance Checklist

To avoid any last-minute stress at the rental counter, make a couple of quick phone calls before you leave for your trip. This little checklist will help you ask the right questions to understand your specific florida car rental insurance requirements.

Questions for Your Auto Insurance Agent:

Does my comprehensive and collision coverage extend to rental cars in Florida?

Will my policy pay for "loss of use," administrative fees, or diminished value if the rental company claims them?

Are my current liability limits adequate for a rental car?

What is my deductible if I get into an accident with the rental?

Questions for Your Credit Card Company:

Is the rental car benefit on my card primary or secondary?

Does the coverage work for rentals in Florida?

Are any cars excluded, like SUVs or minivans? Is there a maximum rental period?

What do I need to do to activate it? (The answer is almost always to decline the rental company's CDW/LDW and pay for the entire rental with that card).

Getting clear answers here will let you walk up to that rental desk with confidence, knowing exactly what coverage you already have and what, if anything, you actually need to buy.

Insurance Tips for International Travelers

Renting a car in Florida is the best way to see the sights, but if you're visiting from another country, the insurance rules can be a bit tricky. The car insurance you have back home, even if it's a great policy, won't cover you on U.S. roads.

This means you'll need to sort out your coverage right at the rental counter. Unlike U.S. residents who might have personal policies that extend to rentals, international visitors almost always need to buy insurance directly from the rental company. It's the simplest and safest way to go.

Why Your Home Country's Policy Won't Work

Think of car insurance as being tied to local laws. A policy from Germany or Australia is built for German or Australian driving laws, not for Florida’s unique no-fault system or the American legal landscape. They just aren't compatible.

Because of this, you can't use your policy from home. Rental companies will require you to buy, at the very least, basic liability coverage before they hand you the keys.

For your own peace of mind, just build the cost of the rental company's insurance into your travel budget. It’s a necessary expense. Trying to skip it could expose you to massive financial and legal trouble, turning a great vacation into a disaster.

The Two Most Important Coverages to Get

As a visitor from abroad, you should focus on two key coverages: the Loss Damage Waiver (LDW) and Supplemental Liability Insurance (SLI).

Loss Damage Waiver (LDW): This one is all about protecting the rental car itself. If the car gets damaged, stolen, or vandalized, the LDW lets you walk away without having to pay for the repairs or replacement. It’s a huge relief.

Supplemental Liability Insurance (SLI): This might be the single most important coverage you can buy. It protects you if you cause an accident that hurts someone or damages their property. SLI boosts your liability coverage way up, often to $1 million. In a country like the U.S., where lawsuits from accidents can be incredibly expensive, this is essential protection.

To get your trip started smoothly, you can find a convenient pickup spot by checking out our various car rental locations.

Documents You'll Need for a Quick Pickup

Having your paperwork in order when you arrive will save you a ton of time. While every company is a little different, you should always be ready to show these four items:

A Valid Driver's License: Make sure it's the one from your home country and has a clear photo of you.

An International Driving Permit (IDP): This isn't always required, but it's a very good idea to have one. It provides an official translation of your license, which can be a huge help.

Your Passport: As an international visitor, this is your main form of ID. You absolutely must have it.

A Major Credit Card: The name on the credit card must match the name of the primary driver on the rental contract.

Getting these documents organized beforehand will help you get on the road fast. Choosing the right insurance from the start gives you the confidence to enjoy every minute of your Florida adventure.

Common Insurance Mistakes And How To Avoid Them

Navigating the world of Florida car rental insurance can feel like trying to solve a puzzle with half the pieces missing. It’s a maze of fine print and confusing acronyms, and even the most seasoned travelers can make simple mistakes that turn a dream vacation into a financial nightmare.

The most common slip-up happens right at the rental counter. In a rush, you either say "yes" to everything offered, likely paying for coverage you already have, or you wave it all off without a second thought, which is just as dangerous. Another big mistake is underestimating your liability needs. Florida's minimums are shockingly low, and a minor fender-bender could easily blow past the $10,000 property damage limit, leaving you on the hook for the rest.

Understanding these common pitfalls is the best way to protect your wallet and keep your trip on track.

The Cost Versus Risk Trap

It’s completely understandable to want to save a few dollars a day by skipping the extra insurance. Who doesn’t want a better deal? But this mindset often trips people into the classic "cost versus risk" trap, where a small daily saving creates a massive financial exposure.

Let's break it down. Declining a Loss Damage Waiver—which usually costs between $10 and $30 a day—means you're personally responsible for every scratch, dent, or major repair. For a week-long trip, you might save $105 by skipping a $15-per-day plan. But if something happens, you could be facing a bill for thousands. You can learn more about Florida's average insurance costs on Experian.com to see how quickly things can add up.

Key Takeaway: Think of that small daily fee as a shield. A minor parking lot mishap or a run-in with a rogue shopping cart could easily cost ten times more than the coverage you turned down.

Hidden Fees That Catch Renters Off Guard

Even if you have solid personal insurance, you might not be completely in the clear. Rental companies have a few extra fees up their sleeves that many personal auto policies simply don't cover. This is where a small accident can turn into a big, nasty surprise on your final bill.

Keep an eye out for these potential charges:

Loss of Use: The rental company can bill you for the daily rental rate for every single day the car is in the repair shop. Their logic? They lost out on potential income while it was out of service.

Diminished Value: This is a charge for the simple fact that a car that's been in an accident is worth less than one that hasn't. You’re paying for the drop in its resale value.

Administrative Fees: You can also get hit with fees for the "hassle"—basically, the paperwork and time it took for them to manage the claim.

Before you confidently decline the rental company's waiver, call your insurance agent and ask them directly if your policy covers these specific fees. A quick phone call can save you from a major financial headache down the road.

By sidestepping these common mistakes, you can make a smart, informed decision that balances cost with real-world peace of mind. To find the perfect vehicle for your protected trip, check out our amazing Cars4Go rental deals today.

Quick Answers to Your Florida Rental Insurance Questions

Even with the basics covered, a few common questions always seem to surface right before a trip. Let's run through them so you can walk up to that rental counter feeling completely confident.

Think of this as your final pre-flight check for rental insurance.

Do I Have to Buy the Rental Company's Insurance?

Nope. Florida law doesn't force you to buy insurance directly from the rental agency. What it does require, however, is that you have proof of the state's minimum liability coverage before you drive away.

You can show this proof in a few ways:

Through your personal car insurance policy, assuming it covers rentals.

With a premium credit card that includes rental car benefits.

By using a separate, third-party rental policy you purchased beforehand.

If you can't show proof of coverage from one of those sources, then yes, you'll have to buy at least the minimum liability plan from the rental company. It's a non-negotiable step to make sure you're legal on Florida's roads.

What Happens If I Get Into an Accident with No Insurance?

Driving a rental car without any insurance is a huge financial risk. If you get into an accident, you're on the hook for 100% of all the costs, personally.

And we're not just talking about a scraped bumper. The financial damage could include:

The full cost to repair or replace the rental car.

Paying for damage to anyone else's property (like their car, a fence, etc.).

Covering medical bills for anyone who gets hurt.

Extra fees the rental company will tack on, like "loss of use" charges for the time the car is in the shop.

These expenses can spiral into tens or even hundreds of thousands of dollars in a flash. It's a gamble you just can't afford to take.

The bottom line is simple: never, ever drive a rental car without confirmed liability insurance. Ensuring you're covered isn't just a smart move; it's essential for protecting yourself from a potential financial disaster.

Will My Credit Card's Insurance Cover Everything?

Almost certainly not. Most credit cards offer what's called "secondary" coverage. This is a bit of a safety net that only kicks in after your primary auto insurance has paid its share. It's usually there to help cover your deductible or other small gaps.

A few high-end travel cards provide "primary" coverage, which is much better because it pays out first. But even then, this coverage is almost always limited to damage or theft of the rental car itself. It very rarely covers liability for damage you cause to others or any medical costs.

Before you rely on it, you absolutely have to call your credit card company and get the exact details of what your specific card covers.

Ready to explore the Sunshine State with total peace of mind? Cars4Go Rent A Car offers transparent pricing, a wide selection of vehicles, and all the information you need to make smart insurance choices. Book your perfect Florida rental car today at https://www.cars4go.com.

Comments